Determining an employee's province of employment is not always a simple task. Find out how you can correctly identify your workers' POE in this guide

Updated August 15, 2024

Establishing an employee’s province of employment (POE) is important to ensure that the proper payroll deductions are withheld. While this may seem straightforward at first glance, determining POE has several layers that payroll professionals must understand to ensure compliance with regulatory requirements.

In this article, Canadian HR Reporter explains how employers can determine a worker’s province or territory of employment. We will dig deeper into the Canada Revenue Agency’s (CRA) criteria, including the recent updates involving full-time remote employees. We will also refer to the National Payroll Institute’s (NPI) POE guidelines to get a clear idea of how the rules apply to real-life situations.

If you’re an employer or payroll professional handling employees across Canada, this guide can help. Read on and learn more about how POE works and what your business should do to remain compliant.

How do you determine an employee’s province of employment?

In its POE guidelines, NPI defines a worker’s province of employment as either:

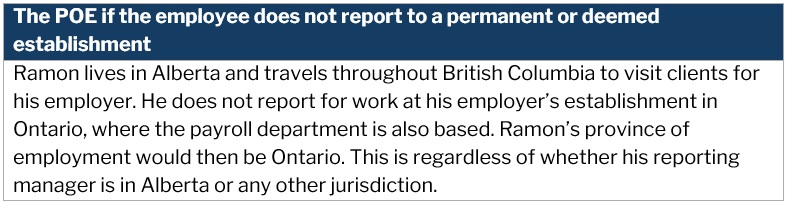

- the province or territory where an employee physically reports for work at any of the employer’s “permanent or deemed establishment”

- the province or territory where the business is located and from which the wages are paid if the employee does not physically report for work

Here are some real-life examples of each scenario:

The CRA and Revenu Québec (RQ), however, provide special considerations on what an establishment is for taxation purposes. These may also qualify as an establishment, according to the tax agencies:

- the use of substantial machinery or equipment at a worksite

- remote employees who have general authority to contract for their employer

Here are some examples:

Note here that Alfred’s employer does not need to own the machinery or equipment for it to be considered as an establishment.

Determining POE is also important for employers paying retiring allowance. A legal expert explains why in this article.

New administrative policy for full-time remote workers

As of January 1, 2024, the CRA has expanded its criteria for employees who are not required to physically report for work at their employer’s establishment. Under the new administrative policy, an employee can be considered reporting for work at an employer’s establishment if:

- a full-time remote work agreement exists

- it is reasonable to consider the employee as “attached to an establishment of the employer”

The policy applies when determining POE for purposes related to:

- Canada Pension Plan/Québec Pension Plan (CPP/QPP)

- employment insurance (EI)

- Québec Parental Insurance Plan (QPIP)

- income tax deductions

It is also aimed at easing the burden for employers and employees by helping them avoid the unintended consequences for provincial tax or benefits administration.

The CRA provided a two-step guide on how to determine the province of employment of full-time remote workers:

Step 1: Determine if a full-time work agreement exists

According to the agency, a full-time remote work agreement is in place if:

- the arrangement can be either permanent or temporary

- the employer allows the employee to work remotely full-time

- the employment duties are performed at one or more locations that are not establishments of the employer

- the employer and employee can justify the existence of the agreement

This policy applies to employees who do not report to work in a physical location, including teleworkers and travelling representatives.

Step 2: Assess if there is reasonable attachment to an establishment

If a full-time remote work agreement exists, the next step is determining whether a worker is “reasonably attached to an establishment of the employer.” This step involves an assessment of facts related to the worker’s situation, which the CRA categorizes as primary and secondary indicators.

Primary indicator

The primary indicator is whether the employee would physically report for work at an establishment if not for the full-time remote work arrangement. Employees who previously came to work in an establishment before the remote work agreement was in place are often considered as attached to that establishment. This is unless their circumstances or the nature of their jobs have changed.

Secondary indicators

The CRA also provided a list of secondary considerations that can help an employer assess a worker’s attachment to their establishment:

- the establishment is where the employee attends in-person meetings

- the establishment is where the employee receives work-related materials or equipment

- the establishment is where the employee gets instructions regarding their duties

- the establishment is responsible for supervising the employee as indicated in the contractual agreement

- the establishment is aligned with the nature of the employee’s duties

These indicators must all be reviewed to determine whether the employee has reasonable attachment to an employer’s establishment. For a worker to be considered as reasonably attached, these indicators must be aligned with their employment situation.

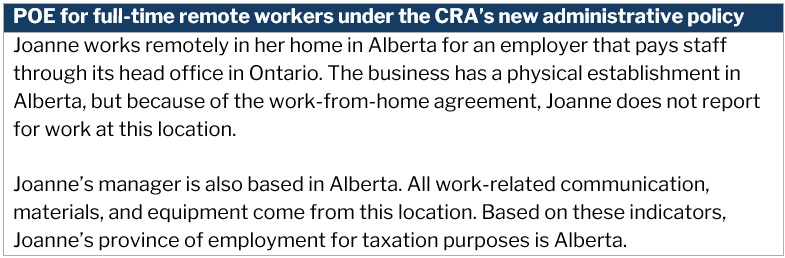

Here’s an example:

The CRA warns that a worker’s reasonably attached status cannot be used to avoid source deductions or employer contributions in a province or territory.

This interactive tool from the agency can help employers determine the province of employment of their employees.

New administrative policy for full-time remote workers in Québec

RQ also updated its parameters for determining a full-time remote worker’s POE. The changes also took effect on January 1, 2024. Québec’s new administrative policy is now aligned with that of the CRA.

Previously, POE for employees under a remote work agreement were based on the business’ location in Québec where they reported or from which they were paid. Under the new policy, the province of employment is determined by the jurisdiction where the worker is most reasonably attached to an employer’s establishment.

What’s the difference between province of employment and province of residence?

Generally, a worker’s province of employment is the province or territory where the employer’s establishment is located and from which employee wages are paid. It is where pension plan and employment insurance contributions and income tax deductions are based.

An employee’s province of residence is the province or territory where they live on December 31 of a taxation year. The CRA uses this information to calculate a worker’s taxes and credits correctly.

“Employees are set up in an organization’s payroll based on their province of employment,” explained Rachel Dobrin-De Grâce, vice-president of government relations and legislative compliance at NPI. “This then dictates the tax rates, source deductions, and year-end reporting that must be applied by law.

“However, an employee’s province of employment may be different from the province of residence, and different still from the province under which this employee is covered for employment/labour standards, pension legislation, and workers’ compensation.”

She also warned employers to never assume that a worker’s province of residence is the same as their province of employment.

“When an employee files a personal income tax return, the province of taxation will revert to the province in which they are a resident on December 31 of a given taxation year.”

Why is it important to determine an employee’s POE?

An employee’s payroll withholdings are based on their province of employment. Determining a worker’s POE is important as this ensures that they are getting the appropriate deductions. Their POE also dictates which federal and provincial or territorial TD1 form they use.

“Determining the province of employment of employees may seem a rather simple task; yet it can be one of the most complex areas of payroll administration,” said Dobrin-De Grâce. “In actual fact, payroll is a profession based on legislative compliance where organizations need to ensure they are compliant with more than 191 federal and provincial regulatory requirements that govern the payroll function.

“An employer is required to calculate and remit source deductions for the following based on the employee’s province of employment: Canada/Québec Pension Plan (C/QPP), Employment Insurance (EI), Québec Parental Insurance Plan (QPIP) and income taxes.

“Employees should be asked to complete a Personal Tax Credits Return (TD1) based on the province of employment. A Source Deductions Return (TP-1015.3-V) should be completed if the province of employment is Québec.”

If you are looking for payroll experts to assist you in matters such as province of employment, our Best in HR Special Reports Page is the place to go. The industry professionals and companies featured in our special reports have been handpicked by their peers. They were also vetted by our panel of experts as dependable and respected market leaders. By partnering with these experts, you can be sure that your payroll processes remain compliant with industry regulations.

Do you have experience with a worker’s province of employment that you want to share? Let us know in the comments.